MEMBERSHIP

AMPLIFY

EN ESPAÑOL

Connect With Us

- Popular search terms

- Automobile

- Home + Renters

- Claims

- Fraud

- Hurricane

- Popular Topics

- Automobile

- Home + Renters

- The Basics

- Disaster + Preparation

- Life Insurance

For the property/casualty (P/C) insurance industry in the first quarter of 2017, the financial weather report (compared with 2016:Q1 and 2015:Q1) was cloudy with occasional bright spots. The clouds: higher CAT claims leading to a deteriorating combined ratio; and continued drop-off in investment yield resulting in a profit slump. The bright spots: stronger net written premium growth; and continued growth in policyholder’s surplus.

For the property/casualty (P/C) insurance industry in the first quarter of 2017, the financial weather report (compared with 2016:Q1 and 2015:Q1) was cloudy with occasional bright spots. The clouds: higher CAT claims leading to a deteriorating combined ratio; and continued drop-off in investment yield resulting in a profit slump. The bright spots: stronger net written premium growth; and continued growth in policyholder’s surplus.

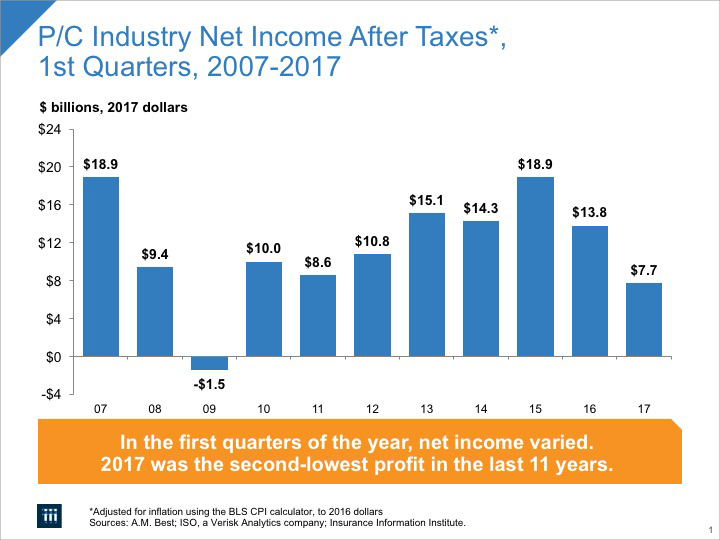

In the eight years since the end of the Great Recession, the first-quarter benchmark for profitability in the P/C insurance industry is the first quarter of 2015, when net income after taxes reached $18.1 billion. Profits in the first quarter of 2016, at $13.4 billion, did not reach that lofty mark, thanks in part to a 6.3 percent rise in incurred claims and adjustment expenses—especially claims from catastrophes—little growth in the U.S. economy and continuing historically low interest rates. These same forces persisted in the first quarter of 2107, resulting in profits of $7.7 billion (Figure 1). In relation to net worth, the industry annualized rate of return on average surplus in 2017:Q1 was 4.4 percent, down from the 7.9 percent posted in 2016:Q1 and down substantially from the 10.8 percent for the first quarter of 2015.

The industry results were released by ISO, a Verisk Analytics company, and the Property Casualty Insurers Association of America (PCI).

Overall, the industry’s performance for the first quarter of 2017 was weaker than the comparable quarter of the prior year. A discussion of the key drivers of the quarter’s performance follows.

Net written premium volume[1] in the first quarter of 2017, at $135.4 billion, grew by 4.0 percent over premium volume in the first quarter of 2016. This is stronger than the 3.2 percent net written premium growth in 2016:Q1 and, remarkably, stronger than the 3.8 percent growth in 2015:Q1. This was the 28th consecutive quarter of all-lines-combined year-over-year net written premium growth—a streak that began in the second quarter of 2010, when the economy was barely beginning its recovery from the Great Recession

Fig. 1

Fig. 2

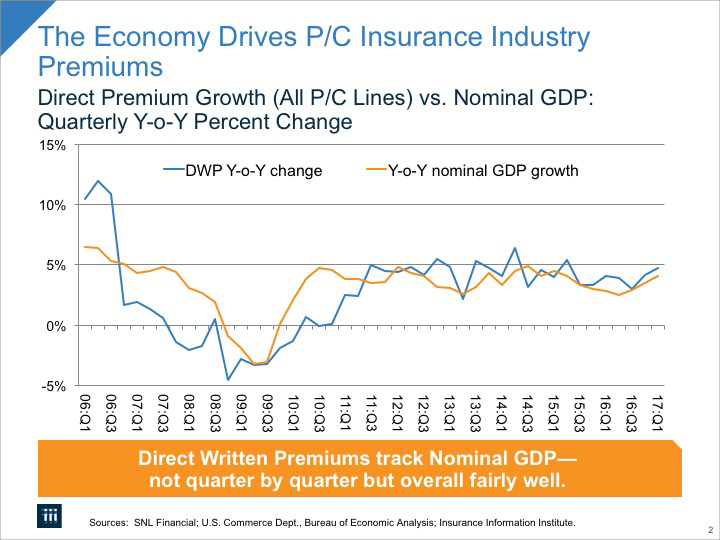

There are two main drivers of premium growth in the property/casualty insurance industry: exposure growth and rate. Exposure growth—basically an increase in the number and/or value of insurable interests (such as property and liability risks)—is driven mainly by economic growth and development.

A summary statistic that corresponds to exposure growth is the nominal GDP. Nominal GDP in the U.S. has, especially since mid-2010, been roughly 4 percent at an annual rate, which correlates with the changes in P/C industry direct premiums (Figure 2). On this basis, the outlook for premium growth is fairly bright: for the full-year 2017, most forecasts currently see nominal GDP growth ranging between 3.9 percent and 4.4 percent, and for the full-year 2018, nominal GDP growth between 3.9 percent and 5.2 percent is expected.

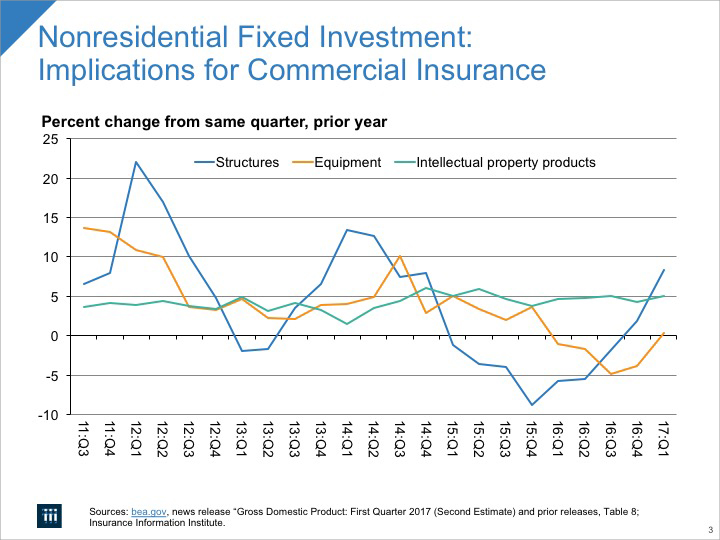

The industry benefitted from exposure growth in some pockets of the economy. In the first quarter of 2017, for example, investment in nonresidential structures rose by 8.4 percent; investment in this category had been negative for all of 2015-16 (Figure 3). The labor market continued improving: the U.S. economy added about 485,000 private sector jobs in the first quarter of 2017, compared to about 520,000 in the same quarter a year earlier. The number of people involuntarily working part-time and those so discouraged that they are not even looking for a job has continued to shrink to levels last seen a decade or more ago in what were considered prosperous times. This job growth is somewhat surprising because, with a “headline unemployment” rate around 4.7 percent during the quarter, some economists judged that we had reached “full employment.” The Institute of Supply Management’s Manufacturing index showed expansion throughout the quarter, and its Non-Manufacturing index was even stronger. With more people working and rising wages, payrolls are expected to continue growing, resulting in rising new premiums written by workers compensation insurers in 2017.

Fig. 3

The other important determinant in industry premium growth is rate activity. Rates tend to be driven by trends in claims costs, conditions in the reinsurance market, marketing and distribution costs, and productivity improvement from investments in technology, among other factors. The effect of claims costs is discussed in the Underwriting Performance section below. Although it is challenging to foresee the interplay of all of these elements as well as macroeconomic factors, it is certainly possible that, if the first quarter increase in loss costs noted below persists, overall industry growth in direct written premiums could keep pace with, or surpass, overall economic growth in 2017.

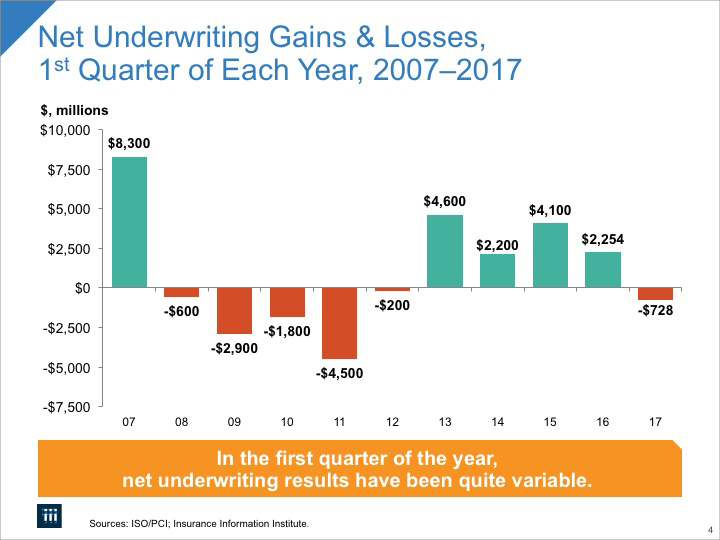

Overall insurance operations (that is, excluding investment performance) is the difference between earned premiums, on the one hand, and the sum of incurred losses, expenses and dividends to policyholders. The first quarter of 2017 produced a loss of $728 million, essentially a break-even status, on earned premiums of $130.8 billion. This follows four straight years of 1st quarter underwriting gains, but that string followed four years of equally large 1st quarter underwriting losses (Figure 4).

Fig. 4

Another widely used industry metric for gauging overall insurance operations is the combined ratio. This ratio is the sum of three percentages: losses and loss adjustment expenses as a percent of earned premiums; policyholder dividends as a percent of earned premiums; and other expenses as a percent of written premiums. In 2017:Q1 this ratio was 99.6, compared to 97.4 in 2016:Q1 (a lower number is better). Normally, a combined ratio under 100 signals an underwriting gain—but not this time. Because the three elements of the combined ratio use different bases (earned vs. written premiums), the combined ratio calculation is not a reliable directional indicator of this quarter’s underwriting results.

There are two main drivers of underwriting performance: losses and loss-adjustment expenses, and other expenses (for marketing, underwriting, and general administration). Losses and loss adjustment expenses grew by $6.4 billion (+7.4 percent) to $93.5 billion—nearly twice as fast as premium growth. Expense growth, at 2.7 percent, on the other hand, was somewhat below the premium growth rate, and close to the overall rate of inflation.

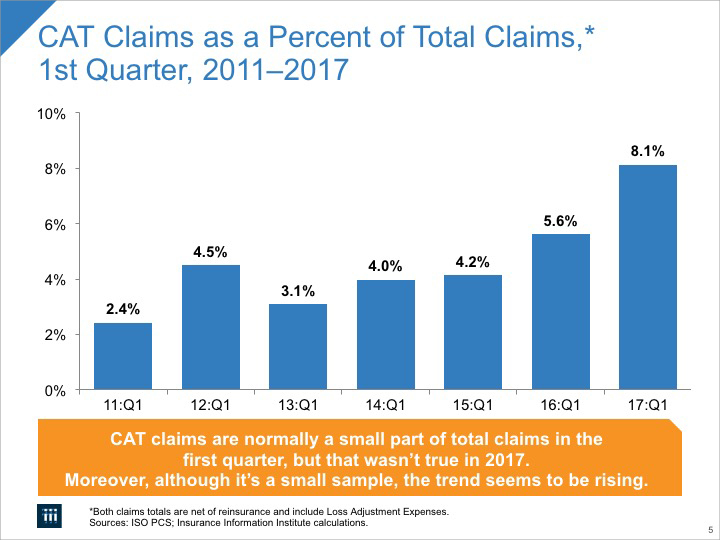

Underwriting performance in the first quarter of 2017 would have been positive but for catastrophe losses that were significantly higher in 2017 than in the prior six years (Figure 5). The first quarter is not normally a high-catastrophe-loss period. ISO/PCI comments that, except for the Northridge earthquake claims in 1994:Q1, over the last 68 years (that is, from 1950 on), the only other time that catastrophe losses topped $4 billion in the first calendar quarter was just a year ago, at $5.0 billion. ISO/PCI estimates that 2017:Q1 catastrophe losses were $7.1 billion. Net losses for non-cat claims also rose but only by $3.8 billion, to $85.9 billion from $82.1 billion—up by 4.6 percent.

Fig. 5

Reserve releases are generally associated with new estimates of expected costs for claims occurring in past years. Overall inflation continues to be remarkably low, likely contributing to these lower estimates, although prices for some items that comprise claims payouts have been increasing at higher rates. For the first quarter of 2017, the industry reported releases of prior year claims reserves totaling $5.5 billion, compared to releases of $4.4 billion in 2016:Q1. Reserve releases contribute to underwriting profit; reserve strengthening would subtract from it.

Driven by the increase in losses and loss-adjustment expenses, but offset to a degree by reserve releases that are larger than last year’s, the industry’s overall combined ratio for the 2017 first quarter deteriorated to 99.6 from 97.4 in 2016:Q1. Combined ratios for the major subsectors of the industry moved in the same direction, but to different degrees. For insurers writing predominantly personal lines, the combined ratio worsened by 0.8 percentage points, to 101.4 percent. For those writing mainly commercial lines (excluding mortgage and financial guaranty insurers), the combined ratio worsened by 1.3 percentage points to 95.6. And those writing balanced books of business posted a combined ratio of 101.3, 5.4 percentage points worse than in the year-earlier quarter.

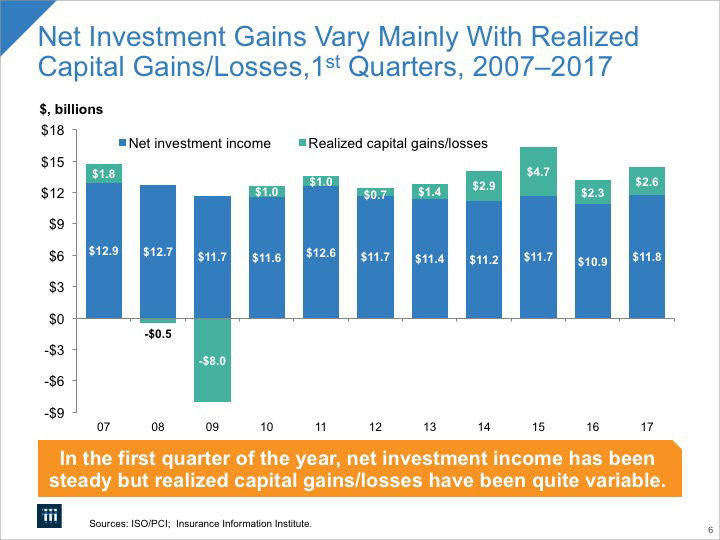

For the first quarter of 2017, net investment gains (which include net investment income plus realized capital gains and losses) were $14.4 billion, vs. $13.2 billion in 2016:Q1 and $16.3 billion in 2015:Q1. The $16.4 billion in net investment gains in 2015:Q1 was a record in this category for first calendar quarters, at least since 1986.

In measuring insurance company net investment gains, accounting rules recognize two components: (i) net investment income; and (ii) realized capital gains or losses. Unrealized capital gains or losses are not considered income and affect only surplus on the balance sheet. Recent patterns in these two components are shown in Figure 6.

Fig. 6

Net investment income itself has basically two elements: interest payments from bonds, and dividends from stock. The industry’s net investment income for the first quarter of 2017 was $11.8 billion, up from $10.9 billion in 2016:Q1, and back to the $11.7 billion in the first quarter of 2015. Most of this income comes from the industry’s bond investments, which are mainly high quality corporates and municipals.

Corporate bond market yields in the first quarter of 2017, as captured by Moody’s AAA-rated seasoned bond index, averaged 3.9 percent, about the same as in the first quarter of 2016. This reflects persistently low inflation and continued weak economic growth. These lower yields continued to shave income off the industry’s bond portfolio despite its growing size. This is because bonds bought before mid-2011 that are maturing now and being reinvested command lower yields than the bonds they replace.

The other significant source of net investment income (besides bond yields) is stock dividends. Stock dividends have risen quite steadily lately. Seasonally adjusted, net dividends in the first quarter of 2017 rose by 2.9 percent over the same quarter in 2016.This is a little faster growth than the 2.3 percent growth rate in 2016:Q1 over 2015:Q1. Stock holdings in general represent roughly only about one-sixth of the industry’s invested assets.

The other significant source of net investment gains is realized capital gains. The broad stock market, as measured by the S&P 500, gained 1.8 percent in January, 3.7 percent in February and lost 0.4 percent in March, providing limited opportunity for cashing gains. As noted, bond yields were fairly steady, dropping slightly in the quarter and offering, in some isolated cases, gains to be seized. The industry realized $2.6 billion in capital gains in 2017:Q1, compared to $2.3 billion in the first quarter of 2016.

Policyholders’ surplus is the excess of assets over liabilities—what in other industries is called “net worth.” Both in dollar terms and in relation to insurance activity, it is a valuable indicator of the strength and capacity of the industry to handle the risk it has accepted.

Policyholders’ surplus as of March 31, 2017 rose to $709.0 billion, up $32.7 billion from $676.3 billion at the end of the first quarter of 2016 (+4.8 percent). According to ISO, a Verisk Analytics company, and PCI, this surplus level is a record for the industry. Most of this gain in surplus occurred during 2016; surplus at year-end 2016 was $700.9 billion, so the 2017 first-quarter gain was, itself, only $8.1 billion (+ 1.2 percent), and most of the gain in 2017:Q1 could be attributed to unrealized capital gains ($6.4 billion).[2]

One commonly used measure of capital adequacy, the ratio of net premiums written to surplus, currently stands at 0.75, close to its strongest level in modern history. The bottom line is that the industry is extremely well capitalized and financially prepared, if necessary, to pay very large scale losses in 2017 and beyond.

The property/casualty insurance industry turned in a profitable performance in the first quarter of 2017. In addition, policyholders’ surplus hit a new record high. Despite a considerable rise in claims, weak economic growth and persistently low interest rates, the industry posted another profitable quarter aided by capital gains and reserve releases. Premium growth, while still modest, is now experiencing its longest sustained period of gains in a decade.

Fundamentally, the P/C insurance industry remains quite strong financially, with capital adequacy ratios remaining high relative to long-term historical averages.

To view the full report from ISO and PCI, click here.

A detailed industry income statement for the first quarter of 2017 follows.

($ billions)

|

*Figures may not add to totals due to rounding. Calculations in text based on unrounded figures.

**Includes mortgage and financial guaranty insurers.

[1]P/C insurers measure premium income in three ways, each of which gives a different insight into the industry’s activity. Direct premiums are amounts that policyholders pay. This is a basic gauge of “retail” activity. Net written premiums are calculated by subtracting amounts insurers pay for reinsurance from direct premiums, and are therefore a simple gauge of the net amount of risk that insurers planned to assume. Net earned premiums are derived by adjusting net written premiums to reflect the insurance actually provided.

[2]This assumes that $5.4 in stockholder dividends came directly from $7.7 billion in net income after taxes, so the contribution to surplus from profits was “only” $2.3 billion.

Download the PDF of Commentary on First Quarter 2017 Results