MEMBERSHIP

AMPLIFY

EN ESPAÑOL

Connect With Us

- Popular search terms

- Automobile

- Home + Renters

- Claims

- Fraud

- Hurricane

- Popular Topics

- Automobile

- Home + Renters

- The Basics

- Disaster + Preparation

- Life Insurance

Don’t be intimidated by specialized insurance language. Below you’ll find definitions of some of the most common terms used when dealing with auto insurance.

An insurance company employee or contractor who reviews the damages and injuries caused by an accident and okays claims payments.

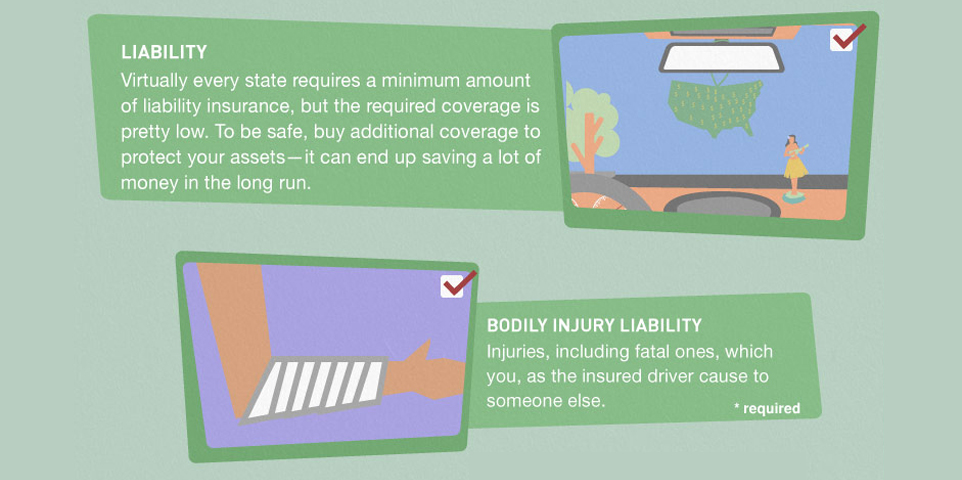

Usually mandated by state law, this insurance provision covers costs associated with injuries and death that you or another driver causes while driving your car.

The formal request to an insurer for payment under the terms of your policy.

Optional coverage that reimburses you for damage to your car that occurs as a result of a collision with another vehicle or other object—e.g., a tree or guardrail—when you’re at fault. While collision coverage will not reimburse you for mechanical failure or normal wear-and-tear on your car, it will cover damage from potholes or from rolling your car.

Coverage against theft and damage caused by an incident other than a collision, such as fire, vandalism, hail, flood, falling rocks and other events.

A confidential ranking developed by insurance companies based on your credit history that may be used to determine the cost of your insurance policy. A good credit score—an indication of responsible money management—has been shown to be a good predictor of whether someone is more likely to file an insurance claim.

The amount subtracted from an insurance payout that you are responsible for. For instance, if you have a $500 deductible for your collision coverage, and an accident causes $2,000 of damage to your car, you pay $500 and your insurance covers the remaining $1,500. There is no deductible for your liability coverage.

Driving in a way that reduces that chance of an accident. Defensive driving techniques include maintaining a safe following distance, scanning the road ahead, keeping both hands on the wheel and much more. If you take a defensive driving course, you may be able to get a discount on your auto insurance.

The value of a car after it has been in an accident and repaired. Even though the car may look fine, it is worth less than its value before the accident. If you’re the victim of an accident, you may be able to collect payment for the diminished value of your car, beyond the repair costs.

Driving your car while distracted is dangerous and often illegal. Texting and using your phone are the most well-known distractions, but fiddling with your radio, looking at a map or GPS system, eating and drinking, talking to passengers and applying makeup also take your eyes off the road—and raise the risk of getting in an accident. Traffic tickets for texting or using your phone, as well as accidents caused by distracted driving, can drive up your insurance rates.

As soon as you drive a new car off the dealer’s lot, its value begins to depreciate. And if you lease or finance the car, you’ll be responsible for the full amount you still owe should something happen to it, but your collision and comprehensive insurance will only cover the actual market value of the car. Gap insurance covers the difference between these two amounts—what the vehicle is worth and what you owe on it. The coverage can be purchased from the auto dealer or directly from your insurance company. For leased vehicles, gap insurance is usually rolled into the lease payments.

Your legal obligation to reimburse others for damage or injury that you cause. Nearly every state requires that you have liability insurance for your car so that if you or someone driving your car causes an accident, the victim will receive appropriate compensation.

Coverage that provides reimbursement for medical expenses for injuries to you or your passengers stemming from an accident where you or someone using your car is at fault. This coverage may also pay lost wages and other related expenses.

Crash parts are those that form the outside “skin” of a vehicle—such as fenders, hoods and doors panels—and are the most frequently damaged in auto accidents. Replacement parts provided by the manufacturer of your car are called original equipment manufacturer (OEM) parts. Parts that are made by another manufacturer are known as generic or aftermarket crash parts and are generally a lower cost, equally safe match for an OEM auto part.

The cost of your insurance policy, payable annually, semiannually or in monthly installments.

Insurance coverage that reimburses others for damage that you or another driver operating your car causes to another vehicle or other property, such as a fence, building or utility pole.

A car is totaled if the cost of repairs exceeds the car’s value. If your car is totaled and you have comprehensive and/or collision coverage, an insurer will pay you the full market value of your car or the limit of the policy, less your deductible if you are at fault.

Extra coverage beyond the limits of your regular liability policies. This will provide an additional layer of protection for your assets in the event you are sued. Your umbrella policy also covers claims that fall under your homeowners insurance policy.

Uninsured motorist coverage will reimburse you when an accident is caused by a driver who lacks insurance—or in the case of a hit-and-run. In the case of a serious accident, underinsured motorist coverage will make up the difference between your losses and the coverage limit of the policy held by the driver who causes the accident.